- Value Investor Daily

- Posts

- Value Investor Daily #23

Value Investor Daily #23

Is value investing dead?

Value investing, the strategy of purchasing undervalued stocks with solid fundamentals and holding them long-term, was established by Ben Graham and championed by legends like Warren Buffett and Charlie Munger.

Some argue that this approach is becoming obsolete in an era where technology and innovation dominate the market.

Let’s examine the relevance of value investing in today's market and explore whether it remains a viable strategy for discerning investors.

The Current State of Value Investing

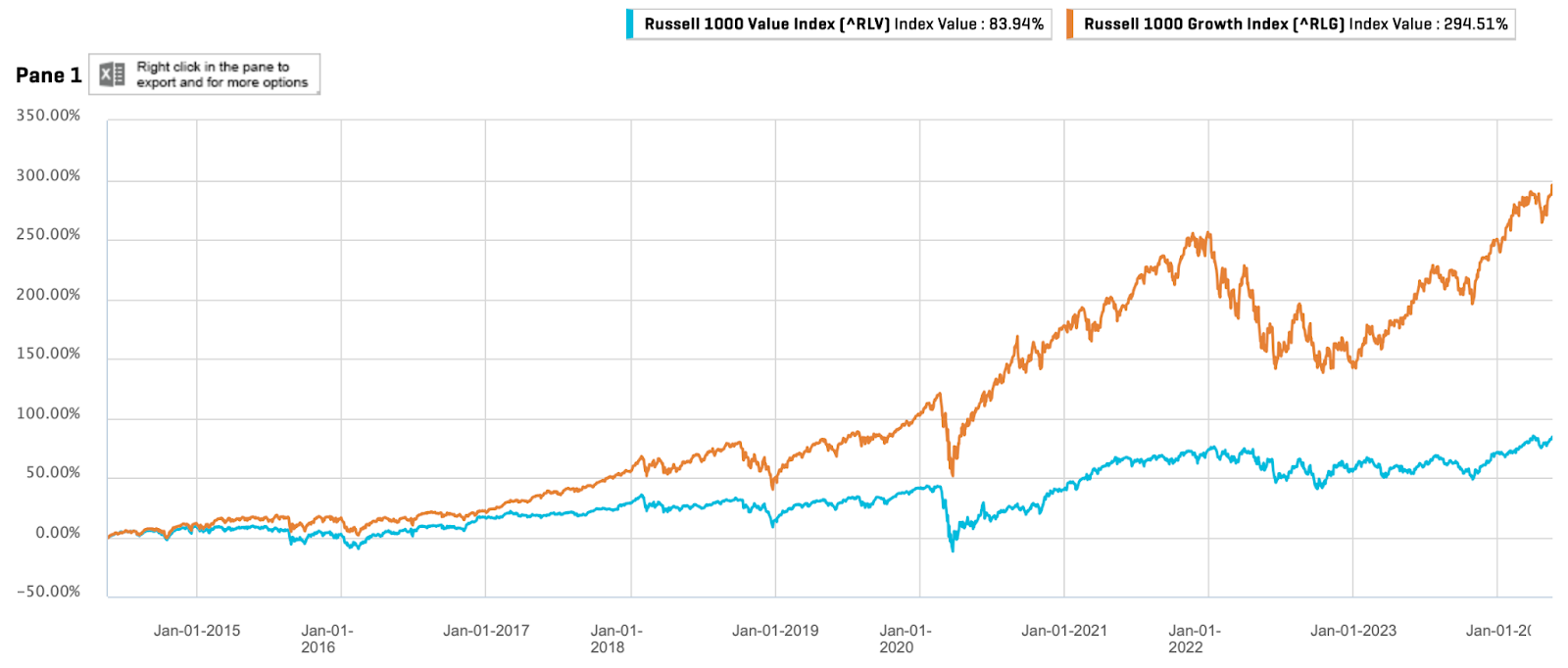

Recent performance metrics illustrate the challenges facing value investors. In 2023, the Russell 1000 Value Index significantly underperformed the Russell 1000 Growth Index, with growth stocks yielding over a 42% return compared to around 11% for value stocks.

Over the past five years, growth stocks achieved an impressive annualized return of 19.5%, while value stocks returned 10.9% annually.

Source: CapitalIQ

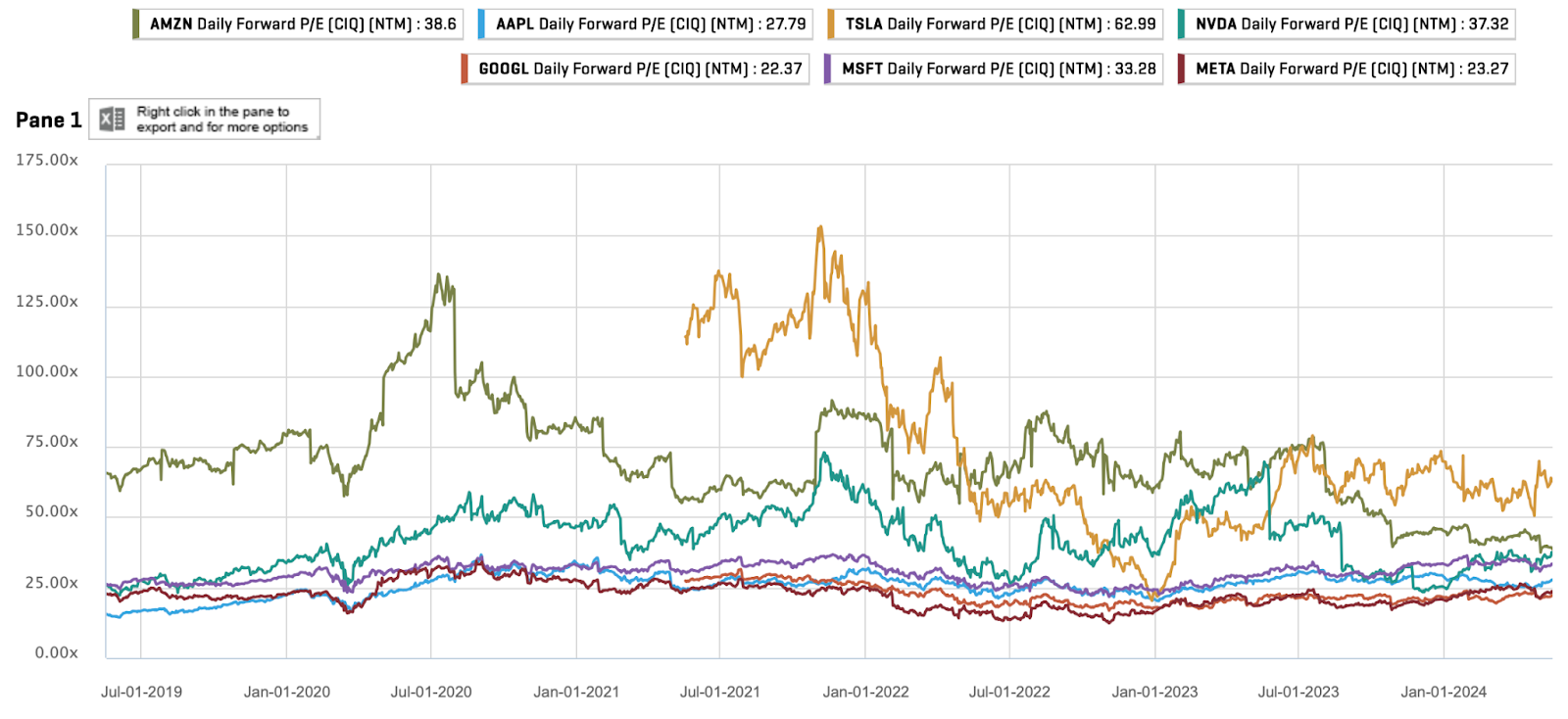

The dominance of growth indices, led by the "Magnificent Seven" (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla), demonstrates that high valuations can be justified by substantial long-term growth.

Notably, once deemed excessively overvalued, companies like Amazon and Nvidia have proven exceptional investments.

The chart below highlights these companies' high forward PE ratios over the last five years. Just a few years ago, 30-150x forward earnings ratios were not uncommon for these tech giants.

Source: CapitalIQ

Even Charlie Munger's favorite, Costco (COST) stock, is richly valued, trading 52x earnings.

Source: Seeking Alpha

So, is value investing officially dead?

Despite market evolutions, the foundational principles of value investing—acquiring stocks at a discount to their intrinsic value—remain relevant.

However, the definition of "value" may need to evolve to incorporate factors such as innovation potential, market dominance, and adaptability to technological advancements.

Lessons from History

Even Buffett had to move from Graham’s style (discount to book value) to Munger’s playbook (discount to future cash flows).

Value investing has endured periods of underperformance before rebounding, as seen during the late 1990s dot-com bubble. But when that bubble burst, value investing surged, underscoring its cyclical nature.

Check out Berkshire’s performance vs. the NASDAQ, Dow Jones, and S&P 500 since 1999.

Source: Trading View

It’s the same destination, with less drawdown, for a higher risk-adjusted return.

This historical cycle suggests that value investing outperforms during periods of economic uncertainty or high inflation when stable cash flows from value stocks become more attractive.

Ultimately, investing success depends on your psychology. Can you stay in long enough to see your money compound? When you chase momentum, eventually, you’re faced with reality. Most can’t stomach an 80% drawdown.

And that’s precisely why value investing will never be dead. Because bubbles, manias, and crashes will always be part of markets.

Human nature isn’t changing anytime soon. That means Mr. Market will occasionally hand you golden opportunities on a silver platter.

So consider a balanced approach that integrates both value and growth strategies. That’s ultimately what’s led Buffett to decades of continued success.

While traditional value stocks with low price-to-earnings ratios can present opportunities, paying premiums for companies with exceptional growth prospects and defensible competitive advantages can also be prudent.

Buffett’s Apple Investment: A Case Study

Warren Buffett’s investment in Apple exemplifies the nuanced approach of modern value investing.

Historically averse to technology stocks, Buffett recognized Apple’s potential as a consumer brand with a loyal customer base and significant recurring revenue streams.

In May 2016, when Apple's shares had lost nearly a third of their value in a month due to a sales drop, Buffett seized the opportunity and invested. At the time, Apple’s P/E was just over 10x earnings.

Since then, Apple’s stock has soared by more than 735%. Apple trades for almost 30x earnings now, and while Buffett has taken some chips off the table, he’s not selling his entire $135 billion stake.

Why? Because he thinks the stock has a durable competitive moat, is still capable of outperformance, and will likely be higher 10-20 years from now.

This case underscores value investing is not solely about low price-to-earnings ratios but about identifying intrinsic value and future growth potential.

Should Everyone Follow Buffett?

While Warren Buffett’s success in value investing is legendary, replicating his approach may not be practical for all investors. Buffett’s deep business acumen, patience, and access to substantial capital enable him to make unique investments. Additionally, his reputation allows him to secure favorable deals.

Most investors should adopt a balanced strategy that blends value investing principles with a readiness to embrace growth opportunities.

This diversified approach, particularly in sectors where innovation and market leadership justify higher valuations, can provide a stable return profile while mitigating risks associated with a non-adaptive, rigid, single investment strategy.

Putting It All Together

For example, you can still rationally invest in the S&P 500. The market is overvalued by some measures, but it’s not in official bubble territory yet, and it’s heavily weighted with big tech exposure.

Then, whenever the market hands you the opportunity for multi-baggers on a silver platter, you can take a small position on those “mispricings.” Don’t go crazy; 5-10% is plenty—because it won’t always work out. The key is to have just a few winners and let them run.

Here’s Meta (META) trading under 10x earnings in 2022, just like Apple did in 2016 when Buffett made his move.

Meta trading cheaper than Apple in 2022. Source: Seeking Alpha

Apple under 10x earnings in 2016. Source: SeekingAlpha

Meta fell almost 80% at the time, even though it was profitable with a strong balance sheet. Do you think it will happen again someday to other great companies? Yes, it will.

What about when absolutely everything looks expensive, even the market at large? You can move some to cash, bonds, or value stocks when you notice signs of a bubble.

Conclusion

As we’ve discussed, there’s a time to index, a time to be more conservative, and a time to concentrate.

With inflation moderating and the Federal Reserve poised to cut interest rates this year, the economic landscape shaped by the COVID-19 era is advancing.

The market is expanding beyond the narrow 2023 rally driven by the "Magnificent Seven" tech giants. As investors look to rebalance and reallocate their portfolios, it may be an opportune time to revisit US value stocks.

This shift in market dynamics suggests that value investing can still play a significant role in contemporary investment strategies.

Value investing is not dead; it is evolving. By recognizing the intrinsic value in a broader context and integrating modern growth factors, investors can continue to leverage this time-tested strategy in a changing market landscape.

Stay ready, and as Buffett says, “Be greedy when others are fearful, and be fearful when others are greedy.”