- Value Investor Daily

- Posts

- Value Investor Daily #31

Value Investor Daily #31

Cracker Barrel, Down 73%, Launches Turnaround Strategy

In partnership with

Cracker Barrel Old Country Store, Inc. (NASDAQ: CBRL), renowned for its blend of homestyle restaurants and gift shops, has faced significant hurdles recently.

Since its peak in Nov 2018, Cracker Barrel's stock has dropped by 73% and is down 37% YTD. This is the second biggest drawdown since the company went public in 1981.

Source:TradingView

This decline reflects broader issues, including a substantial loss of most loyal customers, many of whom have not returned since the pandemic.

Even CEO Julie Felss Masino acknowledged this, stating, "We're just not as relevant as we once were," during a May 16 conference call.

Challenges

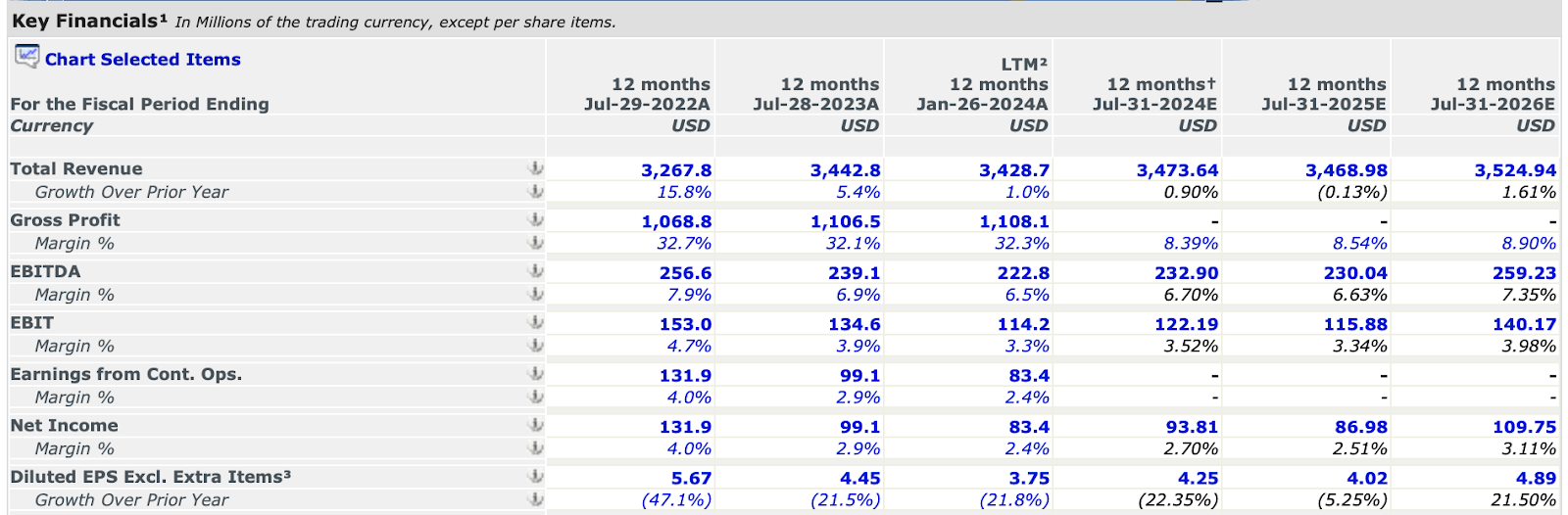

Cracker Barrel's financial performance has been under scrutiny, showing slowing revenue growth and shrinking margins over the past few years.

Source: CapitalIQ

Despite these challenges, there was a positive development as the latest earnings report yesterday (May 30) led to a 6% increase in stock price, driven by optimistic full 2024 year guidance despite mixed Q3 results.

These results included lower-than-expected comparable store and restaurant sales and revenue below consensus estimates.

CEO Julie Felss Masino highlighted the softer-than-expected traffic, underscoring the necessity of executing the company’s strategic transformation plan, which was announced earlier this month.

Positively, for the current fiscal year, Cracker Barrel expects total sales between $3.47 billion and $3.51 billion, slightly higher than the 2023 figure of $3.44 billion and above the Street estimate of $3.47 billion.

Strategic Transformation Plan

Recently, Cracker Barrel announced a strategic transformation plan aimed at revitalizing the brand and recapturing lost customer traffic.

The plan focuses on three key areas: increasing relevance, delivering a food and guest experience that customers love, and enhancing profitability.

Here’s an excerpt from the plan on sales and profitability outlook:

The Company provided a long-term outlook and expects fiscal 2027 sales of approximately $3.8 billion to $3.9 billion and adjusted EBITDA of approximately $375 million to $425 million.

The Company anticipates adjusted EBITDA in fiscal 2025 will be relatively in line with, or slightly lower than, fiscal 2024 results and will then improve in the second half of fiscal 2026 and further accelerate in fiscal 2027.

So we’re looking at a three-year turnaround, at least.

The company generated $3.44 billion in revenue in 2023. If management can produce $3.85 billion of revenue by fiscal 2027 within three years, that’s a CAGR of 3.82%, outpacing inflation expectations by only 1.45%.

But if they can tap operating leverage and deliver $400 million of EBITDA, an all-time high, that’s 67% higher than the $239 million EBITDA delivered in 2023.

But always be wary of statements like these from management. As Charlie Munger says, “I think that, every time you see the word EBITDA, you should substitute the words ‘bull$#!t earnings.’”

To achieve these goals, the company is testing new remodel prototypes and plans to complete 25-30 remodels in fiscal 2025.

The strategy includes brand refinement, menu optimization, evolving the store and guest experience, enhancing digital and off-premise offerings, and improving the employee experience.

As part of these initiatives, the company announced an 80% reduction in dividends over the next three years.

Valuation and Analyst Perspectives

We utilized 15 different valuation methods, such as DDM Multi Stage, Earnings Power Value, EV / EBIT Multiples, Price / Sales Multiples, P/E Multiples, and 5-Year DCF Revenue Exit, to determine the stock's fair value.

The estimated fair value is $60.7, suggesting approximately a 26% upside from the current stock price.

Wall Street analysts also see potential, with price targets ranging from $48 to $90 and an average target of $56.75, indicating a 17.93% upside.

Source: Seeking Alpha

Furthermore, the Relative Strength Index (RSI) of 26.39 indicates that Cracker Barrel stock is in oversold territory. This suggests that the stock price has fallen sharply and may be due for a rebound.

Source: Seeking Alpha

The stock trades for 10.5 times earnings vs. a 5-yr average of 16.8 times.

Conclusion

Despite recent difficulties, Cracker Barrel's strategic transformation plan will be implemented over the next three years. It remains to be seen if they can win back customers and return to sustainable earnings growth.

If you believe in management’s promising guidance, now could be an ideal time to look further into Cracker Barrel stock. If not, you can always turn over more rocks.

Stiff competition and persistent inflation remain strong concerns. A successful turnaround, in this case, will require a lot of work and a lot of things to go right. Don’t expect it to be all smooth sailing, and position accordingly.

As always, do your own research. Thank you for reading today!

The Rising Demand for Whiskey: A Smart Investor’s Choice

Why are 250,000 Vinovest customers investing in whiskey?

In a word - consumption.

Global alcohol consumption is on the rise, with projections hitting new peaks by 2028. Whiskey, in particular, is experiencing significant growth, with the number of US craft distilleries quadrupling in the past decade. Younger generations are moving from beer to cocktails, boosting whiskey's popularity.

That’s not all.

Whiskey's tangible nature, market resilience, and Vinovest’s strategic approach make whiskey a smart addition to any diversified portfolio.

Subscribe to our partners free: