- Value Investor Daily

- Posts

- Value Investor Daily #30

Value Investor Daily #30

3 Energy Companies With Upside

In partnership with

Put your money to work in a high-yield cash account with up to $2M in FDIC† insurance through program banks.

Get started today, with as little as $10.

The continued rapid expansion of artificial intelligence (AI) technology is significantly boosting the overall demand for energy and utilities.

AI’s computational needs are leading to a surge in energy consumption, particularly from data centers that house AI servers, which are highly power-intensive.

As AI continues to grow, its impact on the energy sector becomes increasingly profound, driving substantial changes and creating new opportunities. The demand for energy to run these AI systems is growing at 26-36% per year.

In this piece, we discuss three undervalued companies in the energy and utilities sectors that present compelling buy opportunities.

Exxon Mobil Corporation

Exxon Mobil (NYSE: XOM) is the leading entity in the Oil, Gas & Consumable Fuels industry, specializing in the exploration and production of crude oil and natural gas both domestically and internationally.

Year-to-date, Exxon Mobil's share price has increased nearly 14%, and we believe there is still room for further upside.

Fair Value Analysis:

Using 15 valuation methods, including DDM Stable Growth, Earnings Power Value, P/E Multiples, Price/Sales Multiples, and a 10-Year DCF Revenue Exit, the average fair value estimate is around $136, suggesting a 19.6% upside from the current stock price.

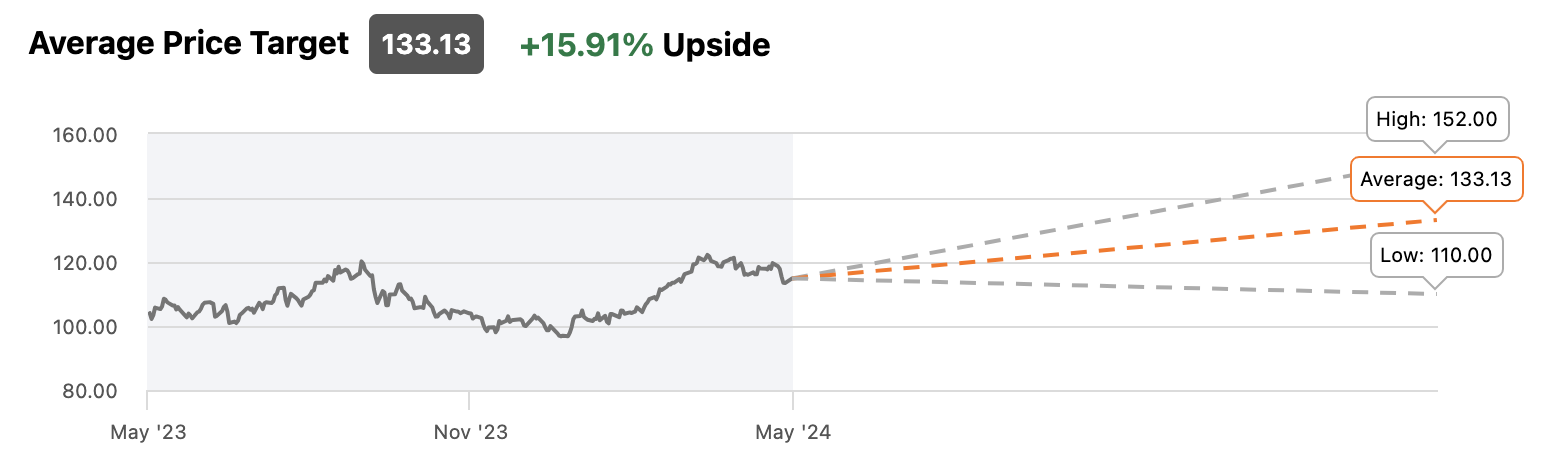

Wall Street Analyst Targets:

Analysts have price targets ranging from $110 to $152, with an average target of $133.13, indicating a 15.91% upside from the current price.

Source: Seeking Alpha

On May 3, Exxon Mobil announced the completion of its acquisition of Pioneer Natural Resources, creating an unconventional business with the largest high-return development potential in the Permian Basin.

Exxon Mobil has maintained dividend payments for 54 consecutive years and raised its dividend for 41 consecutive years, currently yielding 3.35%.

Recently, Morgan Stanley analysts resumed coverage of Exxon Mobil, emphasizing the company's robust growth potential and favorable valuation.

They highlighted Exxon's broad operations across energy, chemicals, and emerging low-carbon sectors, which provide a significant competitive edge and support sustainable growth and a distinctive value proposition.

According to analysts, Exxon Mobil's stock is trading at about a 55% discount to the broader market, nearly twice its historical discount.

This undervaluation persists despite Exxon offering a shareholder return yield of approximately 7% and achieving a cash flow growth rate that is double that of its peers in the energy sector.

These attributes make Exxon Mobil an attractive investment opportunity in the current market.

National Fuel Gas Company

National Fuel Gas (NYSE: NFG) operates as a diversified energy company through four segments: Exploration and Production, Pipeline and Storage, Gathering, and Utility.

Fair Value Analysis:

Using 13 valuation methods, including EV/Revenue Multiples, Earnings Power Value, P/E Multiples, Price/Book Multiples, and a 5-Year DCF EBITDA Exit, the average fair value estimate is around $64.50, implying a 16.7% upside from the current stock price.

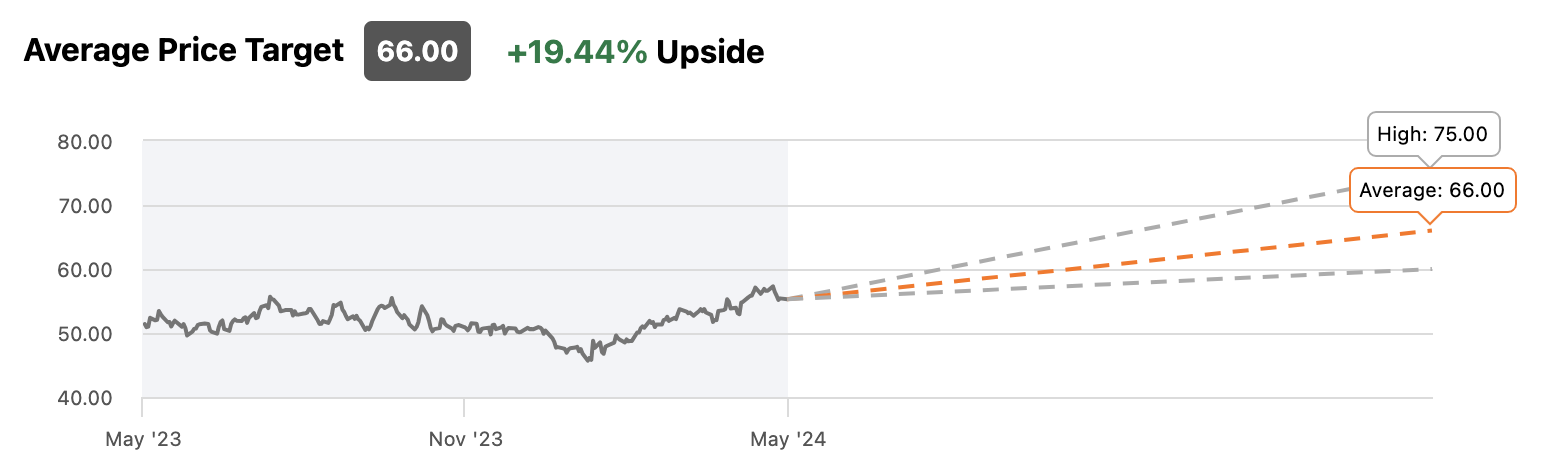

Wall Street Analyst Targets:

Analysts have price targets ranging from $60 to $75, with an average target of $66, indicating a 19.44% upside from the current price.

Source: Seeking Alpha

Earlier this month, National Fuel Gas reported strong second-quarter performance, with adjusted EPS reaching $1.79 per share, a 16% increase from the previous year, exceeding Wall Street estimates.

The company's success was driven by its regulated businesses, which saw a 36% rise in earnings per share, along with a 10% increase in production from Seneca Resources and increased throughput in the gathering segment.

Despite some challenges, National Fuel remains committed to its strategy of hedging through price cycles and is optimistic about future natural gas prices.

The company has also announced a $200 million share buyback program (vs. $5B market cap) and ongoing investments in modernization and expansion projects.

National Fuel has maintained dividend payments for 54 consecutive years and raised its dividend for 53 consecutive years, currently yielding 3.57%.

Energy Transfer

Energy Transfer (NYSE: ET) owns and operates one of the largest and most diversified portfolios of energy assets in the United States, with more than 125,000 miles of pipeline and associated infrastructure.

Fair Value Analysis:

Using 14 valuation methods, including DDM Multi Stage, EV/Revenue Multiples, Earnings Power Value, P/E Multiples, EV/EBIT Multiples, and a 10-Year DCF Growth Exit, the average fair value estimate is around $19, implying a 22.6% upside from the current stock price.

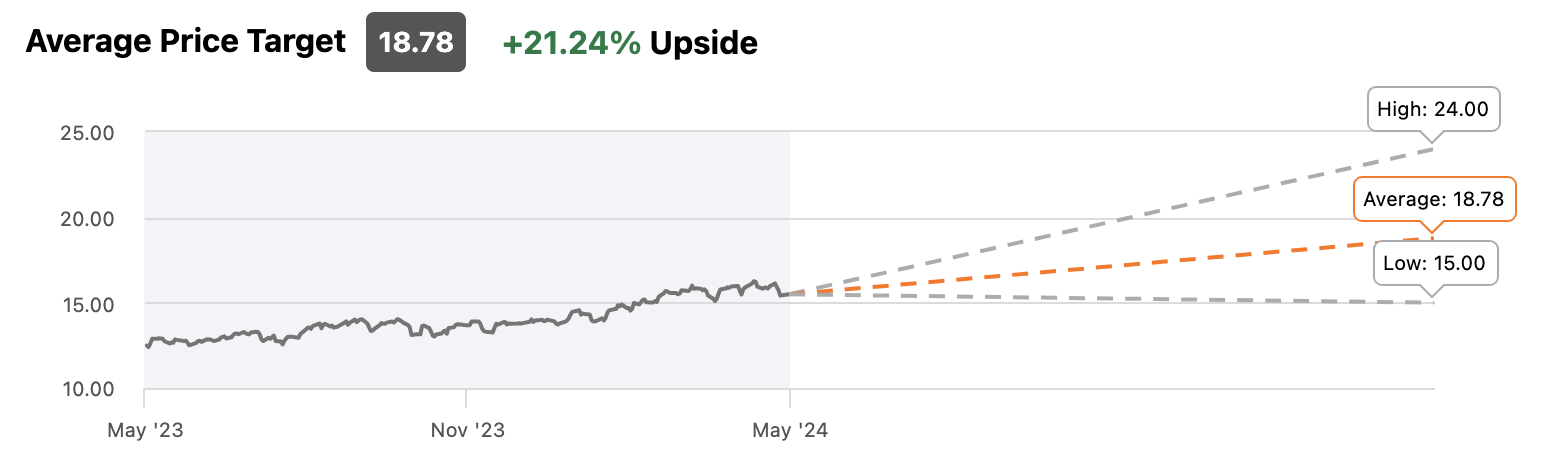

Wall Street Analyst Targets:

Analysts have price targets ranging from $15 to $24, with an average target of $18.78, indicating a 21.24% upside from the current price.

Source: Seeking Alpha

On Wednesday, Energy Transfer and WTG Midstream announced that they have finalized a definitive agreement under which Energy Transfer will acquire WTG Midstream Holdings LLC.

The transaction is valued at approximately $3.25 billion. This acquisition will significantly expand Energy Transfer’s network, adding over 6,000 miles of gas gathering pipelines and eight gas processing plants with a combined capacity of about 1.3 billion cubic feet per day (Bcf/d).

This strategic move enhances Energy Transfer’s overall infrastructure and capabilities in the energy sector.

That’s it for today. Thanks for reading!

Put your money to work in a high-yield cash account with up to $2M in FDIC† insurance through program banks.

Get started today, with as little as $10.

Subscribe to our partners free: