- Value Investor Daily

- Posts

- Value Investor Daily #27

Value Investor Daily #27

Small Cap Value Idea Down 48% YTD: Semler Scientific (SMLR)

Micro Cap Stock Deep Dive: Semler Scientific

In the opportunistic world of micro-cap stocks, Semler Scientific (NASDAQ: SMLR) stands out amidst recent turbulence, experiencing a substantial 48% decline in its shares year-to-date.

However, beneath this apparent setback lies a company with robust fundamentals and promising prospects.

Let's delve into whether this pullback offers a golden opportunity for investors to capitalize on.

Company Profile

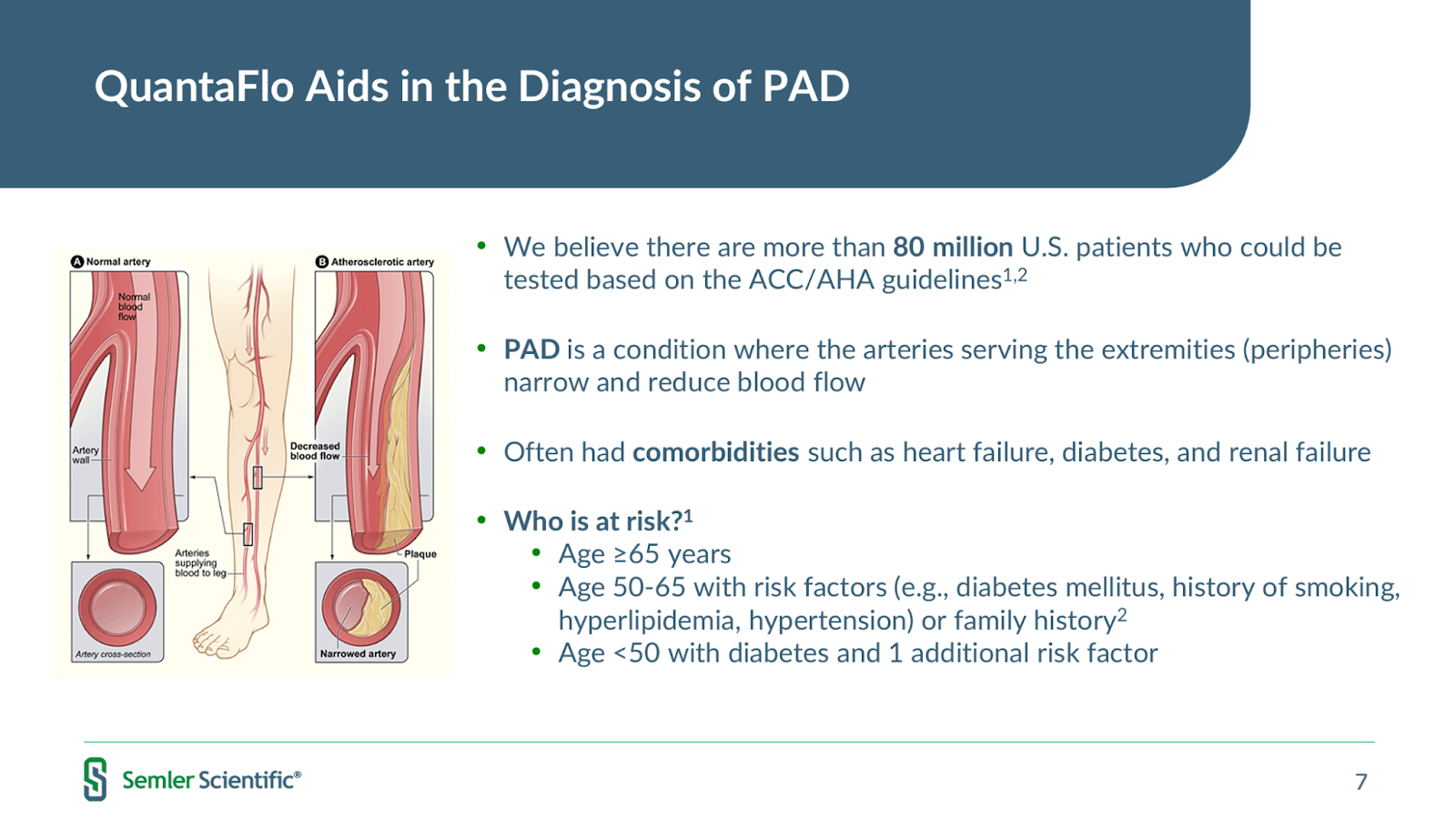

Semler Scientific specializes in developing, manufacturing, and marketing innovative products and services aimed at facilitating the early detection and treatment of chronic diseases.

Among its flagship offerings is QuantaFlo, a revolutionary four-minute in-office blood flow test that empowers healthcare providers to integrate blood flow measurements into their patients' vascular assessments.

Recent Earnings

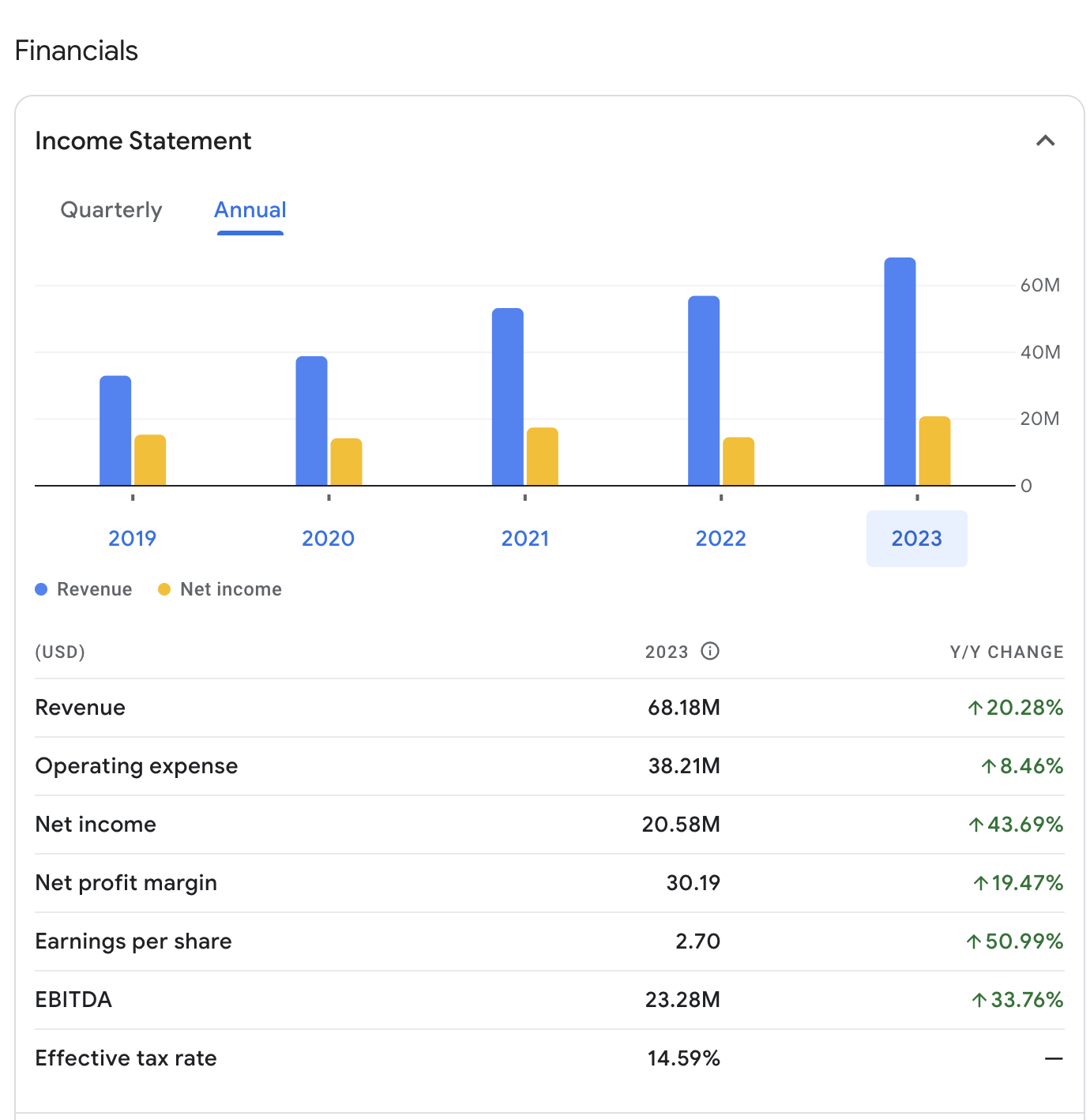

Following its Q1 earnings release on May 7, Semler Scientific witnessed a sharp decline of more than 25% in its share price the subsequent day.

It announced earnings per share of $0.78 in the first quarter, trailing behind average analyst expectations by $0.25, which had anticipated $1.03.

Revenue for the quarter stood at $15.9 million, reflecting a 13% decrease compared to the previous year, in contrast to the anticipated $21.4 million as per Wall Street consensus estimates.

Despite falling short of analyst expectations, the earnings report revealed notable highlights amidst the challenges. While revenue for the quarter decreased by 13% year-over-year, the company still achieved a 22% increase in net income.

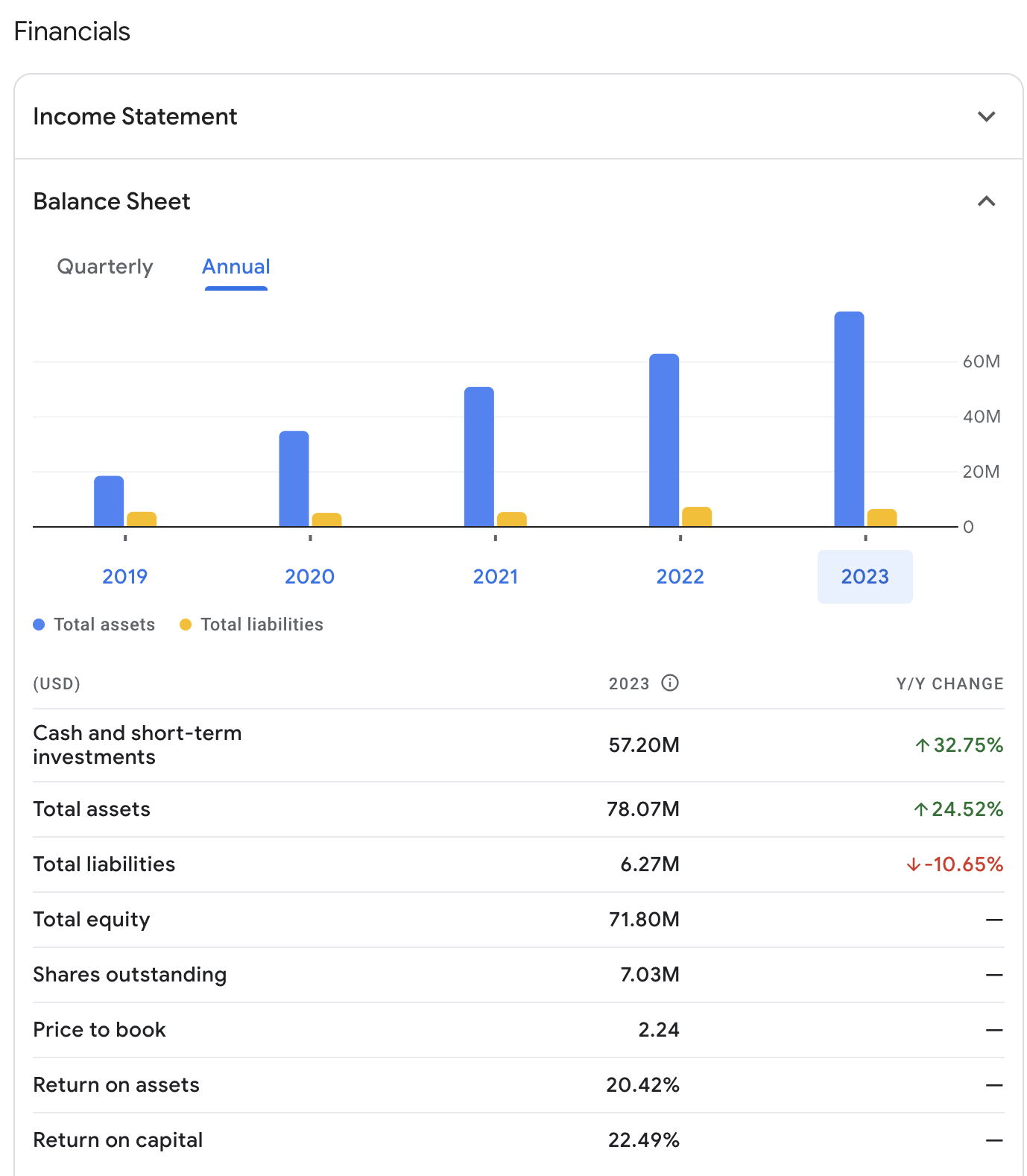

Furthermore, Semler Scientific fortified its financial position with a record balance of cash and cash equivalents amounting to $62.9 million, paving the way for potential share buybacks and strategic initiatives.

Semler Scientific is actively seeking new FDA clearance for its heart dysfunction product scheduled for the second half of 2024, while simultaneously aiming to broaden its customer base for peripheral arterial disease (PAD) testing.

Efforts to expand the customer base for PAD and explore opportunities for inorganic growth are currently in progress.

When asked about potential uses of the cash on the balance sheet, CFO Renae Cormier had this to say:

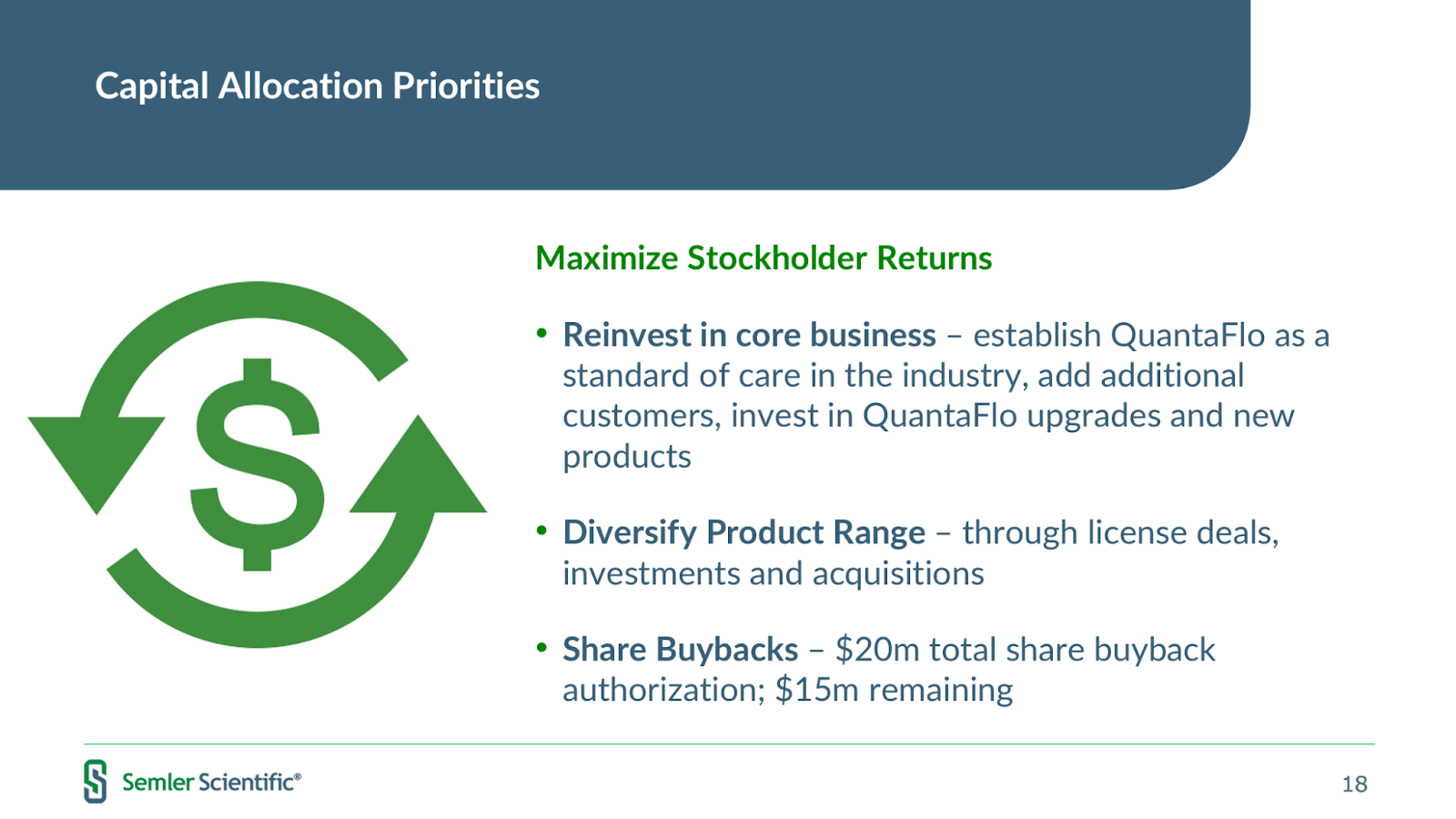

“Sure. So really, when we're looking at our cash, there's kind of three areas that we're looking at: First and foremost is reinvesting back into our product. And so, an example of this is the heart dysfunction 510(k) clearance that we're going after. The second, as you mentioned, is inorganic growth activities.

We do have a robust pipeline. But as you know, these things take time. So, we are going to be very diligent in what we're doing and what we're looking at. Our Board has a lot of experience in capital allocation, and they are closely aligned with management and shareholders in trying to make sure that we carefully approach any acquisition that we may have.

And then the third piece with our cash could potentially be share buybacks. So, we do have a $20 million share buyback that's authorized by the Board. We have bought back $5 million already, so we do have $15 million authorized in share repurchases. So that's something else that the Board will assess -- will assess looking at with capital allocation and depending on the market circumstances.”

Strengths

Semler Scientific boasts attractive valuation metrics, with a low P/E ratio of 8.25 and a compelling PEG ratio of 0.22, signaling potential undervaluation relative to its earnings growth prospects.

Management's aggressive share buyback initiatives and consistent earnings growth averaging a 28.62% five-year CAGR underscore the company's commitment to enhancing shareholder value.

Additionally, Semler Scientific's debt-free balance sheet and substantial cash reserves, constituting approximately 74% of its total asset base, instill confidence in its financial stability and flexibility.

Fair Value

Utilizing an extensive range of valuation techniques, such as Price/Book Multiples, 5Y DCF EBITDA Exit, 5Y DCF Revenue Exit, 10Y DCF Growth Exit, EV/Revenue Multiples, P/E Multiples, and Price/Sales Multiples, we have determined Semler Scientific's fair value estimate to be $33.53.

This assessment suggests a potential 31% margin of safety.

Analyst Perspective

Currently, Semler Scientific is covered by a sole analyst, who has assigned it a Strong Buy rating and a price target of $40. This projection implies a substantial 74.37% upside potential from the present price level.

Source: SeekingAlpha

Conclusion

Despite its recent share price decline, Semler Scientific stands out as an idea worth exploring. With its strong financial position, strategic growth initiatives, and favorable valuation metrics, the company appears undervalued in the current market environment.

The current weakness in its stock presents a strategic buying opportunity in a company with long-term potential. Do your own research and decide if it makes sense to you.

Subscribe to our partners free:

Are you enjoying these emails?

Do you have comments, suggestions, or questions? We’d love to hear from you. Just hit reply and fire away.

Thank you for reading!