- Value Investor Daily

- Posts

- Value Investor Daily #22

Value Investor Daily #22

CVS Plunges on Earnings Miss. Loses $30 Billion Market Cap. Is This an Undervalued Opportunity?

CVS Health (NYSE: CVS) experienced a significant drop in its share price, falling approximately 17% on May 1 following its first-quarter earnings report for 2024.

The earnings failed to meet market expectations, and the company lowered its guidance. Since the beginning of the year, CVS shares have declined by more than 27%, resulting in a market cap loss exceeding $30 billion. Shares are down 50% from their peak.

Source: TradingView

Earnings Review

For Q1, CVS Health reported an EPS of $1.33, missing the analyst estimate of $1.71. This shortfall was mainly due to underperformance in the Health Care Benefits segment, which struggled with utilization pressures in its Medicare business. The company’s revenue for the quarter was $88.4 billion, below the Street estimate of $89.33 billion.

Looking forward, the company revised its annual guidance, now expecting a minimum adjusted EPS of $7.00, down from its previous forecast of at least $8.30. This is also below the consensus of $8.28. The revision reflects ongoing utilization pressures in the Health Care Benefits segment that are expected to persist throughout the year.

Despite these lowered expectations, CVS remains committed to improving margins. CVS currently has a TTM PE ratio of 9.80x earnings, with a forward PE of 7.6x, indicating significant investor skepticism about the company’s growth prospects.

The revised $7.00 EPS guidance assumes a (2)%-(3)% Medicare Advantage margin and does not account for any potential improvement over time.

While short-term challenges persist due to higher utilization, no perceived value is attributed to potential margin stabilization in Medicare Advantage or the company's CostVantage plan.

Notably, a 100 basis point improvement in MA margins could add $650 million to $700 million to operating earnings, and stabilizing Pharmacy EBIT margins could contribute an additional $250 million annually.

Although the path forward may be turbulent, the risk/reward profile appears favorable at current levels. Additionally, CVS offers a dividend yield of 4.75%.

Analyst Opinions

Following the earnings report, several Wall Street firms, including TD Cowen, UBS, Leerink Partners, and Cantor Fitzgerald, downgraded their ratings on CVS. Additionally, analysts from Argus, Wells Fargo, Morgan Stanley, Goldman Sachs, Barclays, and several others reduced their price targets on the stock.

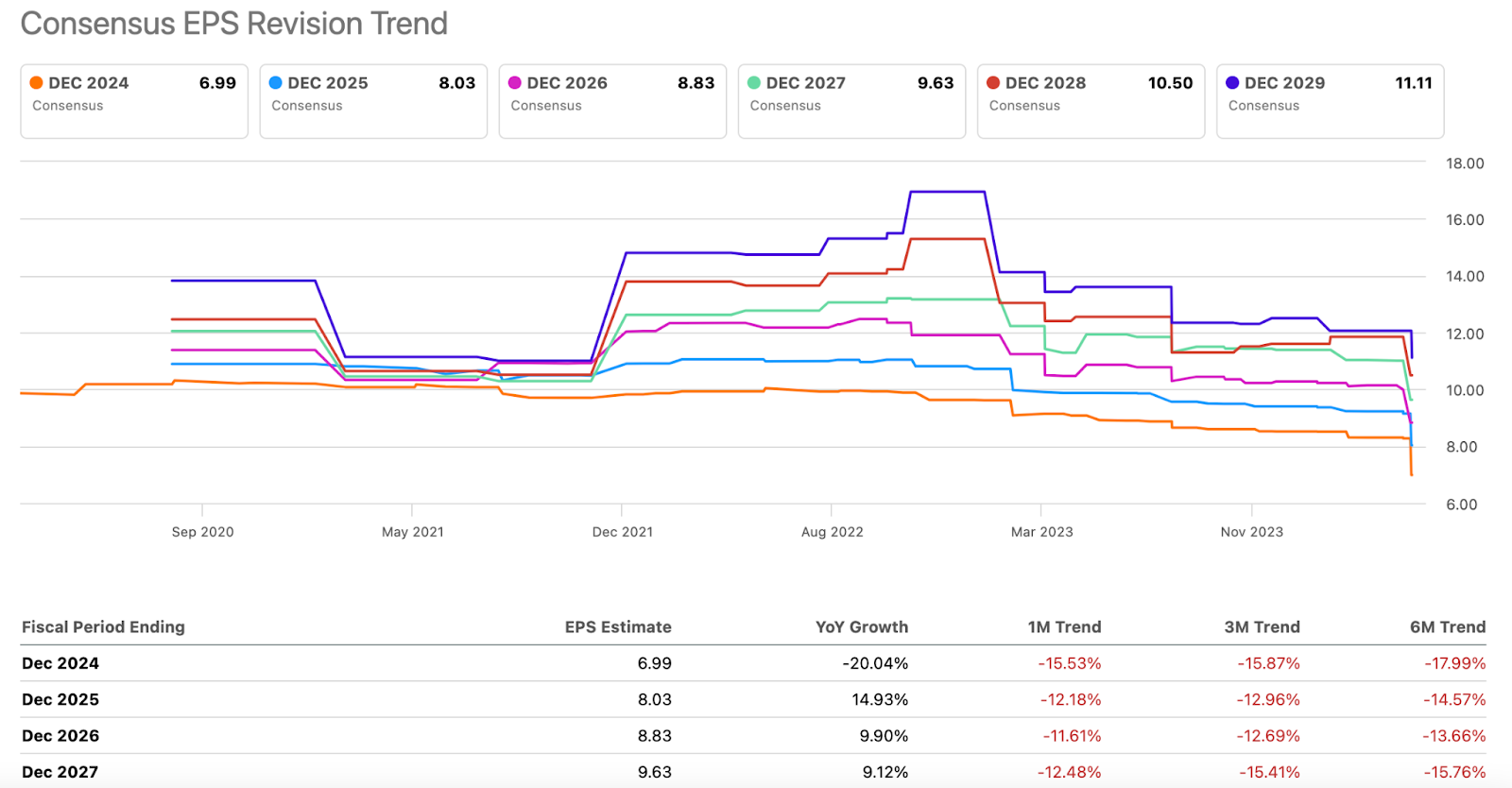

The Consensus EPS Revision Trend shows significant downward revisions to EPS estimates by Wall Street analysts following CVS's recent earnings report.

Source: Seeking Alpha

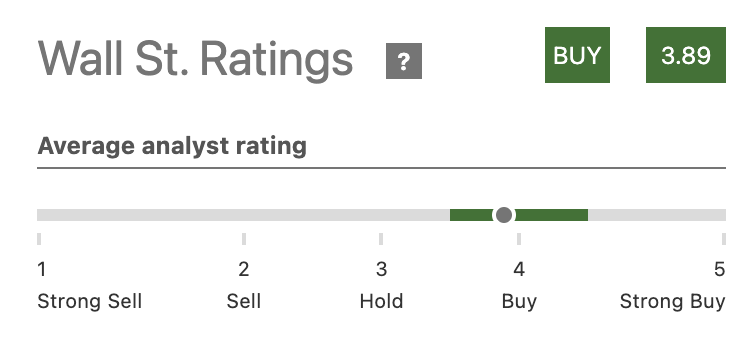

Despite these downgrades, the consensus among analysts still leans towards a Buy rating for CVS.

Source: Seeking Alpha

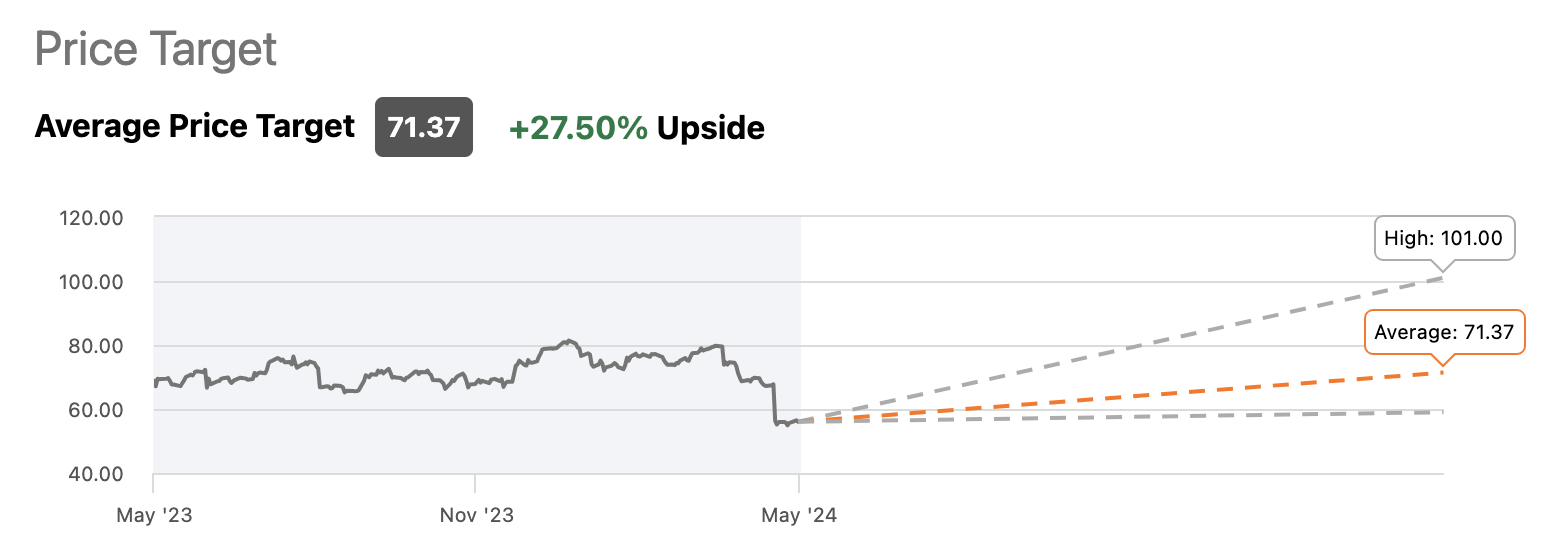

The price targets range from $59 to $101, with an average target of $71.37, suggesting a potential upside of approximately 27% from the current stock price.

Source: Seeking Alpha

Technical Analysis

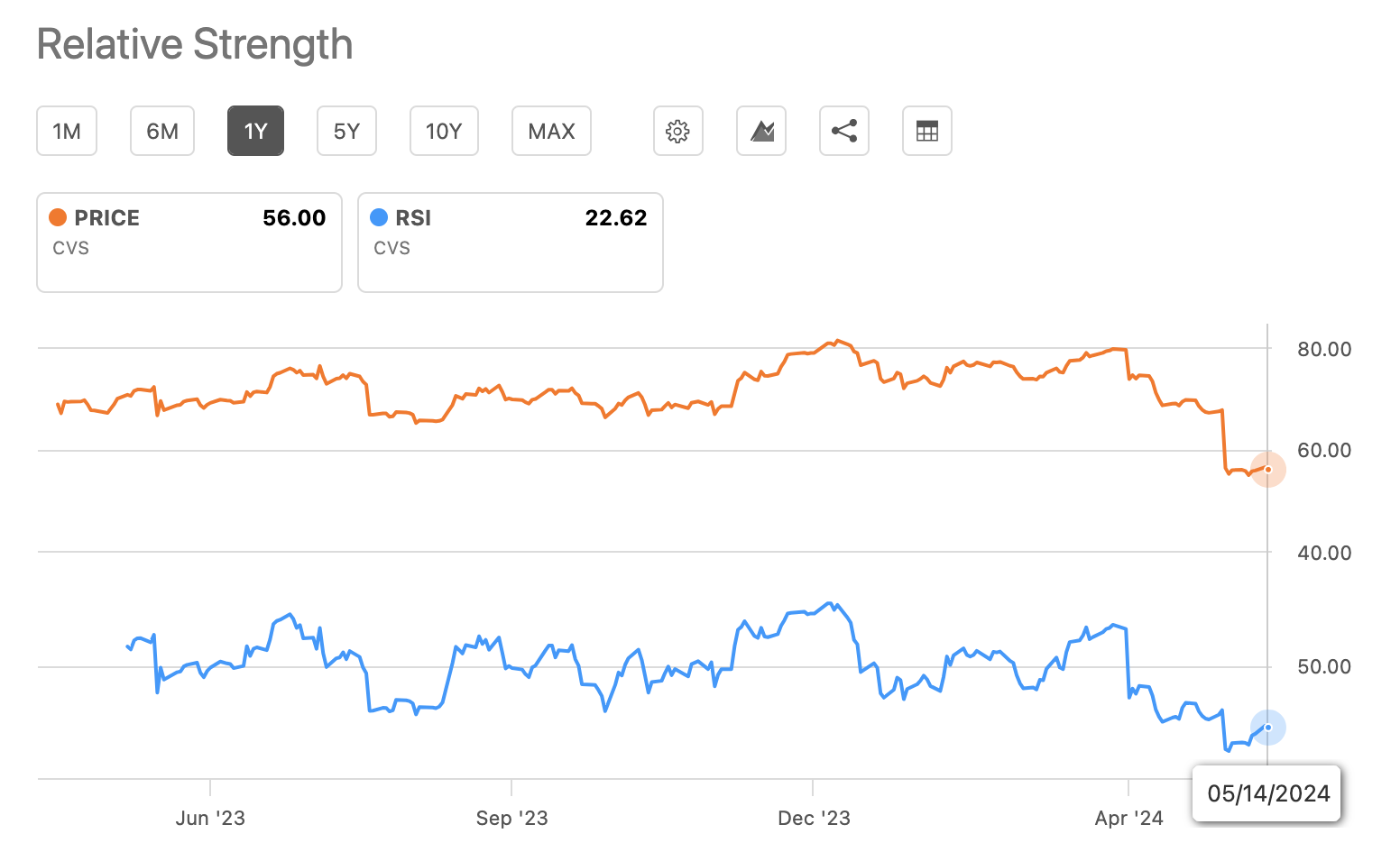

CVS's Relative Strength Index (RSI) of 22.62 indicates that the stock is in oversold territory. An RSI below 30 generally suggests that a stock's price has fallen sharply and could be poised for a rebound.

Source: Seeking Alpha

Valuation Estimates

We used several valuation methods to estimate the fair value for CVS:

P/E Multiples: $62.56

EV/EBITDA Multiples: $73.69

EV/EBIT Multiples: $77.06

Price/Book Multiples: $75.31

EV/Revenue Multiples: $83.60

Price/Sales Multiples: $76.77

DDM Multi-Stage: $55.39

5-Year DCF EBITDA Exit: $103.77

The average of these estimates is around $76, implying a potential upside of approximately 35% from the current stock price.

Conclusion

Given CVS's strong fundamentals, its current valuation presents a potentially attractive entry point for investors willing to navigate the near-term challenges.